Can Advisors Thrive Amid Contrasting Market Outlooks?

Advisors face an equity market landscape marked by opportunity and challenge. The near-term outlook for 2025 has many strategists forecasting double-digit gains for U.S. equities, driven by robust earnings growth, resilient consumer demand, and innovation in sectors like AI. Potential policy tailwinds like tax cuts and decreased regulation further support optimism.

But beyond 2025 (and maybe sooner), a different reality emerges—one of subdued returns, shaped by high valuations, slower economic growth, global uncertainties, persistent inflation, and rising long-term rates.

Adding to this complexity are rumbling risks of market volatility, fueled by global trade tensions, macroeconomic uncertainty, and geopolitical challenges. Advisors are left navigating a delicate balance: seizing the opportunities of a potentially strong 2025 while preparing portfolios for the headwinds that may define the years to come.

Let’s explore:

-

- The drivers behind 2025’s optimism, including forecasts of 10%+ equity returns from firms like Goldman Sachs.

- The longer-term outlook for equities, tempered by structural challenges.

- Actionable strategies for advisors to help clients thrive in both environments.

Optimistic 2025 Outlooks for U.S. Equities

What’s Driving 2025’s Optimism?

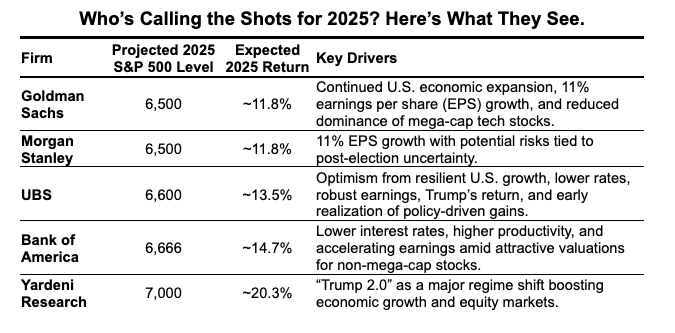

The near-term picture appears bright for U.S. equities, according to the major investment firms projecting strong returns for 2025. Double-digit gains are on the table, as strategists point to several key factors driving this optimism:

Why Do Major Firms Predict Double-Digit Returns for 2025?

-

- Earnings Growth: Analysts predict sustained increases in corporate earnings, fueled by business momentum and a business-friendly administration.

- Policy Support: Assuming legislative cooperation, new tax breaks may drive growth. Regulatory relief will also favor business.

- Economic Expansion: Expectations of steady GDP growth, improved productivity, and lower short-term policy rates are a supportive backdrop for corporate performance and confidence.

- Moderate Inflation and Interest Rates: Controlled inflation and favorable monetary policy can sustain financing conditions and consumer purchasing power.

- Technological Innovation: Advances in AI and other cutting-edge technologies are driving productivity and opening new market opportunities.

Source: “The S&P 500 Is Forecast to Return 10% in 2025,” Goldman Sachs, 11/26/24. (link); “Morgan Stanley Raises Base Case 2025 Year End S&P 500 Target to 6,500,” Reuters, 11/18/24. (link); “More to Go in Stocks,” UBS, 12/13/24. (link); “BofA Global Research Expects 2025 to Be a Year of Further Equity Market Strength Amid Macro Uncertainty,” BofA, 12/3/24. (link); “Ed Yardeni Sees ‘a Lot of Upside’ in U.S. Stocks,” ThinkAdvisor, 12/30/24. (link). Note, expected returns are calculated based on 1) 2024 year-end level of S&P 500, 2) each firm’s projected target level for the S&P 500 at the end of 2025, and 3) the current dividend level of 1.24% for the S&P 500.

Source: “The S&P 500 Is Forecast to Return 10% in 2025,” Goldman Sachs, 11/26/24. (link); “Morgan Stanley Raises Base Case 2025 Year End S&P 500 Target to 6,500,” Reuters, 11/18/24. (link); “More to Go in Stocks,” UBS, 12/13/24. (link); “BofA Global Research Expects 2025 to Be a Year of Further Equity Market Strength Amid Macro Uncertainty,” BofA, 12/3/24. (link); “Ed Yardeni Sees ‘a Lot of Upside’ in U.S. Stocks,” ThinkAdvisor, 12/30/24. (link). Note, expected returns are calculated based on 1) 2024 year-end level of S&P 500, 2) each firm’s projected target level for the S&P 500 at the end of 2025, and 3) the current dividend level of 1.24% for the S&P 500.

Long-Term Expectations: Prepare Now

The Long View: Why Advisors Need to Prepare for the Decade Ahead

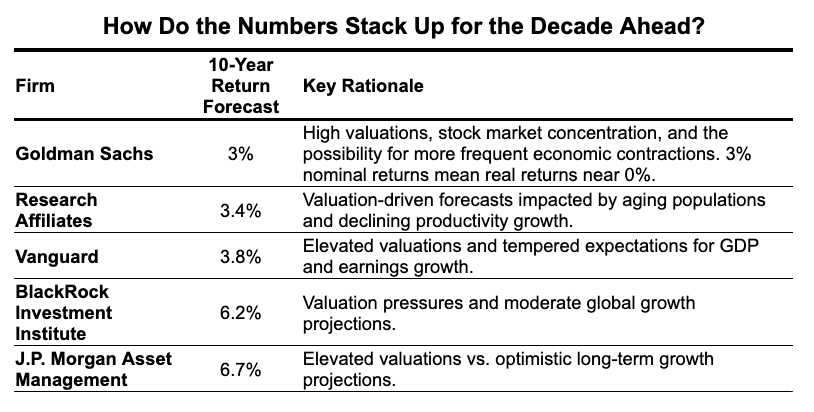

While the 2025 projections above offer expectations for equity gains, the long-term picture paints a more cautious story. Across the board, leading asset managers—including Vanguard, Goldman Sachs, and BlackRock—forecast U.S. equity returns to land in the low-to-mid single digits over the next decade. The Goldman Sachs ten-year forecast of 3% nominal returns for equities equates to a 0% to 1% real return depending on the path of inflation. This contrasts starkly with the average ~13% annualized returns over the past decade and long-term historical averages of ~11%, highlighting a significant reset in expectations.

What Might Hold Back Long-Term Equity Returns?

-

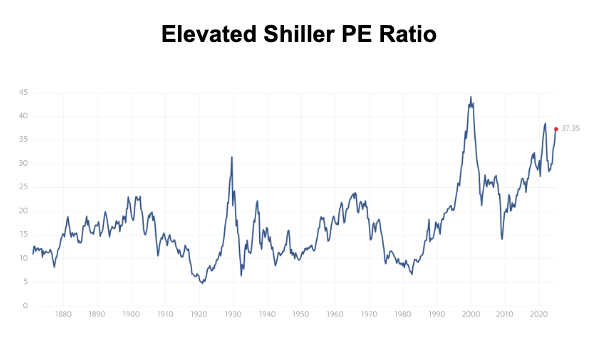

- High Valuations—Ceiling for Future Growth: Elevated starting valuations leave little room for further price-to-earnings (P/E) multiple expansion. The current Shiller P/E ratio of 37.35—exceeded only during the dot-com bubble in 1999—raises concerns about equity levels. Historically, such high valuations have preceded prolonged periods of subdued returns, including the infamous “lost decade.”

Source: Multpl. Market, financial, and economic data as of Dec. 2024

Source: Multpl. Market, financial, and economic data as of Dec. 2024

-

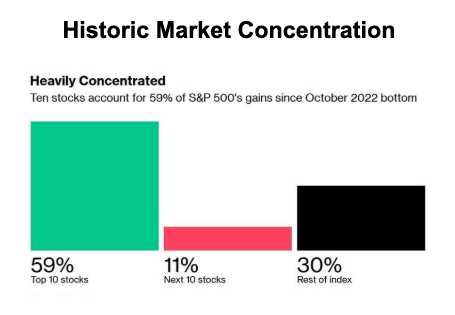

- Market Concentration and Lack of Breadth: A small group of mega-cap tech stocks have dominated market performance. According to Bloomberg, only 10 stocks provided 59% of the gains of the S&P 500 since the October 2022 low. While their outperformance has driven recent gains, this high concentration creates fragility.

Source: Bloomberg. Numbers may not add due to rounding.

Source: Bloomberg. Numbers may not add due to rounding.

-

- Debt Dynamics—Pressures Mounting:

-

- Debt and Deficits: The U.S. national debt recently topped $36 trillion after the government posted a $1.9 trillion deficit in fiscal 2024. U.S. Treasury issuance will keep upward pressure on long-term rates for the foreseeable future.

- Interest Rate Divergence: For the first time in history, longer-term interest rates rose 100 basis points after the Fed cut short-term rates by 100 bps, signaling investor concerns over rising deficits and persistent inflation.

- Bankruptcies and Defaults: Business bankruptcies rose 33.5% in 2024, exceeding the pandemic total in 2020. The leveraged loan default rate hit 4.7% in 2024, also ahead of the 2020 pandemic year rate of 4.5%. Nevertheless, investor complacency is keeping spreads tight and volatility low in the credit markets.

-

- Slower Growth—Structural Headwinds:

-

- Demographics as Destiny: As populations age, workforce growth slows, placing a natural drag on economic productivity and demand—regardless of advances in AI and technology

- Moderate GDP Growth: Slower global and domestic growth rates weigh on corporate earnings potential.

-

- Rising Volatility—A More Uncertain Environment: Geopolitical tensions and evolving global trade conflicts raise the risk of market instability. Macro risks, ranging from inflationary pressures and rising commodity prices to unstable currency exchange rates, are creating an environment where volatility may not be just a risk but a near certainty.

- Debt Dynamics—Pressures Mounting:

Source: “Global Strategy Paper: Updating our long-term return forecast for US equities to incorporate the current high level of market concentration,” Goldman Sachs, 10/18/24. (link); Research Affiliates (link); “Vanguard Capital Markets Model® forecasts,” Vanguard, 12/5/24. (link); “BlackRock Investment Institute | Capital Market Assumptions,” November 2024. (link); “J.P. Morgan Unveils 2025 Long-Term Capital Market Assumptions, Highlighting Strong Foundations for 60/40 Portfolios and Opportunities to Enhance Returns Through Active Management and Alternatives,” PRNewswire, 10/21/24. (link).

Source: “Global Strategy Paper: Updating our long-term return forecast for US equities to incorporate the current high level of market concentration,” Goldman Sachs, 10/18/24. (link); Research Affiliates (link); “Vanguard Capital Markets Model® forecasts,” Vanguard, 12/5/24. (link); “BlackRock Investment Institute | Capital Market Assumptions,” November 2024. (link); “J.P. Morgan Unveils 2025 Long-Term Capital Market Assumptions, Highlighting Strong Foundations for 60/40 Portfolios and Opportunities to Enhance Returns Through Active Management and Alternatives,” PRNewswire, 10/21/24. (link).

Navigating Mixed Signals

Advisors face a critical balancing act: capitalizing on the near-term opportunities of a potentially strong 2025 while preparing portfolios for the headwinds of the decade ahead. This environment calls for prompt and thoughtful preparation, a focus on diversification, and strategies designed to perform in a variety of market conditions.

Steps Advisors Can Take Now:

-

- Prepare for a Lower-Return, More Volatile Environment: Set realistic client expectations for long-term returns. Emphasize the need for diversified portfolios that can withstand higher market swings while maintaining a focus on long-term goals.

- Consider Risk-Managed Equity Strategies: Incorporate strategies with built-in hedges to reduce downside risks while allowing participation in market upside. These can be valuable tools in periods of volatility or uncertainty:

-

- Reducing the downside of equities can enhance long-term returns while improving the client experience.

-

- Explore Uncorrelated Strategies That Prosper from Volatility: Global macro strategies, which capitalize on opportunities across asset classes—commodities, currencies, equities, and fixed income—offer diversification and potential outsized returns in volatile environments:

-

- Through commodity strategies, macro managers seek to transform geopolitical and inflation risk into excess returns.

- Currency markets enable traders to tap into opportunities arising from global trade, interest rate differentials, and international fiscal and inflation dynamics.

- Global macro strategies are cash-efficient and generally carry high excess cash after implementing any derivatives. Thus, higher rates offer improved yields on excess collateral and contribute to higher total returns. In the world of macro, higher interest rates also offer expanded trading opportunities.

-

With equities unlikely to carry portfolios alone, exploring alternative strategies is more critical than ever.

+ + +

THE OPINIONS EXPRESSED ARE THOSE OF THE AUTHOR OR THE INDIVIDUAL TO WHOM THE STATEMENTS ARE ATTRIBUTED. WHILE BELIEVED TO BE REASONABLY BASED ON FACT AND INQUIRY, THERE CAN BE NO GUARANTEES THAT SUCH OUTCOMES EXPRESSED OR IMPLIED HAVE OCCURRED OR WILL INDEED OCCUR.

THIS DOCUMENT IS NOT A SOLICITATION FOR INVESTMENT. SUCH INVESTMENT IS ONLY OFFERED ON THE BASIS OF INFORMATION AND REPRESENTATIONS MADE IN THE APPROPRIATE OFFERING DOCUMENTATION. ANY INVESTMENT PROGRAM DESCRIBED HEREIN IS SPECULATIVE, INVOLVES SUBSTANTIAL RISK AND IS NOT SUITABLE FOR ALL INVESTORS. NO REPRESENTATION IS BEING MADE THAT ANY INVESTOR WILL OR IS LIKELY TO ACHIEVE SIMILAR RESULTS.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.